Close

Close

Enter your shipment number.

Close

Foreign Trade Zones vs. Bonded Warehouses: What’s Right for You?

Both offer tariff mitigation strategies for shippers importing goods into the U.S., but there are critical differences between the two...

4 August 2025

Foreign Trade Zone (FTZ) Overview

Foreign trade zones (FTZs)—also known as free trade zones—are specially designated areas within the U.S. that operate outside of normal customs protocols, allowing companies to temporarily avoid import taxes or completely under certain conditions.

The goal of an FTZ is to incentivize companies to make products in the U.S. that tariffs and other barriers might have otherwise encouraged them to make elsewhere, to employ American workers for supply chain functions like storage and handling, and to create more efficient supply chains for manufacturers who export often.

Duty is deferred until the goods exit the FTZ and enter U.S. commerce. The applicable duty rate is the rate in effect when the goods are admitted into the FTZ and must be entered as Privileged Foreign (PF) status. Some federal laws do not apply to merchandise admitted to FTZs.

- FTZs are regulated by the U.S. Foreign-Trade Zones Board and U.S. Customs & Border Protection (CBP).

- FTZ sites are generally required to be located within or adjacent to a U.S. CBP port of entry. FTZ sites may be located within CBP port of entry boundaries, or 60 statute miles of the port of entry’s outer limits, or a 90-minute drive from the outer limits of a CBP port of entry. Certain subzones may be located further distances from the port of entry boundaries at CBP’s discretion.

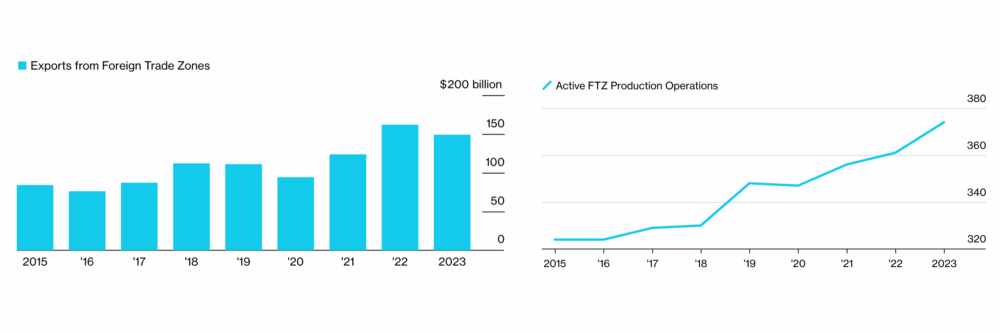

Data Shows that Foreign Trade Zones Have Become Increasingly Critical Among International Trade

FTZs have been a key enabler of U.S. exports as the number of active FTZ operations has climbed since the first USA/China trade conflict in 2018/2019.

Source: Foreign Trade Zones Board annual report to Congress.

Bonded Warehouse Overview

A bonded warehouse is a facility that’s secured and supervised by U.S. Customs & Border Protection (CBP) where imported goods can be stored without duty payment until they’re withdrawn. Considered within U.S. Customs territory; all federal laws apply to merchandise entering a bonded warehouse.

- Bonded warehouses are usually located within a short distance (+/- 35 miles) of a CBP port of entry, which allows for efficient movement of goods during import and export processes.

- Duty is paid when goods are withdrawn for consumption in the U.S. using the duty rate in effect on the withdrawal date.

Types of Bonded Warehouses

There are different classes of bonded warehouses:

- Class 1: Merchandise undergoing examination by Customs, under seizure, or pending final release from Customs custody.

- Class 2: Importers’ private bonded warehouses are used exclusively for the storage of merchandise belonging or consigned to the proprietor thereof.

- Class 3: Public bonded warehouses used exclusively for the storage of imported merchandise.

- Class 4: Bonded yards or sheds for the storage of heavy and bulky imported merchandise; stables, feeding pens, corrals, or other similar buildings or limited enclosures for the storage of imported animals; and tanks for the storage of imported liquid merchandise in bulk.

- Class 5: Bonded bins or parts of buildings or elevators to be used for the storage of grain.

- Class 6: Warehouses for the manufacture in bond, solely for exportation, of articles made in whole or in part of imported materials or of materials subject to IRS tax; and for the manufacture for home consumption or exportation of cigars in whole of tobacco imported from one country.

Manufacturing can occur only in a Class 6 bonded warehouse for export.

- Class 7: Warehouses bonded for smelting and refining imported metal-bearing materials for exportation or domestic consumption.

- Class 8: Warehouses for the purpose of cleaning, sorting, repacking, or otherwise changing condition, but not manufacturing, imported merchandise.

- Class 9: Duty-free stores

- Class 11: General order warehouses

Note: Classes 1, 2, 3, 4, 5, 6, 7 or 11 may also be approved by CBP for manipulation activities like Class 8. The distinctions between manipulation and manufacturing may be significant and complex.

Features

- Bond Requirements

- Duty Avoidance

- Duty Deferral

- Foreign vs. Domestic

- Storage Duration

- Tariff Classifications

- Value-Added Services

Bonded: No importer/entry bond is required, but an FTZ operator bond is required.

FTZ: Proprietor must have a proprietor’s bond, and each entry must be covered by either a single or continuous importer/entry bond.

Bonded: Duties paid only if goods enter U.S. commerce.

FTZ: If goods are re-exported or scrapped, no duties are owed.

Bonded: Duties are paid only when goods are withdrawn from the warehouse.

FTZ: Duties are deferred until goods enter the U.S. market.

Bonded: Generally, only dutiable imported merchandise and/or merchandise subject to a quota may be admitted.

FTZ: Both foreign and domestic may be admitted.

Bonded: Up to 5 years

FTZ: Unlimited

Bonded: Duty/tariff rates are paid based on the date of the bonded warehouse withdrawal.

FTZ: Different zone statuses allow classification and duty/tariff payment either in condition of merchandise as admitted to FTZ (PF Status) or in condition of merchandise upon withdrawal from FTZ (NPF Status).

Note: All trade remedy actions (i.e., Reciprocal Tariffs, IEEPA, Section 301, Section 232, Section 201, AD/CVD) mandate that imported merchandise be admitted to FTZs in PF Status, thereby solidifying the duty/tariff rates associated with that merchandise at the time of FTZ admission and preventing traditional FTZ inverted tariff/duty reduction benefits.

Additionally, merchandise subject to Antidumping (AD)/Countervailing (CV) duties must be admitted in PF Status, but AD/CVD duties are assessed at the rate in effect at the time of entry for consumption from the FTZ.

Bonded: Limited activities such as repacking and labeling

FTZ: Expanded capabilities include assembly, kitting, and storage

Merchandise Handling

FTZs: FTZs can have domestic and foreign merchandise stored together in the activated area, and merchandise of both types can be combined in an FTZ.

Inventory can be managed by Lot # or by UIN (Part Number/ SKU) with depletion under FIFO or FOFI methodology.

Bonded Warehouses: Bonded warehouses may only store imported dutiable merchandise in the active bonded warehouse area and therefore cannot combine foreign and domestic merchandise.

Inventory can be managed by Lot # or, with approval from U.S. Customs, by UIN (Part Number/SKU) with depletion under first-in-first-out (FIFO) methodology. Combining different types of merchandise is restricted.

Withdrawals for U.S. Consumption

FTZ: Importers may utilize FTZs during weekly entry procedures to withdraw merchandise for U.S. consumption, which may provide considerable financial savings and logistics benefits.

Bonded Warehouses: No weekly entry options! Withdrawals are individualized per bonded warehouse entry, which is feasible for some companies and commodities but not as much for others.

Transfers Between FTZ/Bonded Warehouses

- FTZ merchandise in non-privileged foreign (NPF) status can be transferred for entry into a bonded warehouse with certain date restrictions; however, merchandise in privileged foreign (PF) status cannot be entered into a bonded warehouse from an FTZ.

- Bonded warehouse entered merchandise can only be transferred for admission to an FTZ for exportation or destruction in Zone Restricted (ZR) Status.

Related content

-

Tariff Updates

This is an evolving situation—tariff rates, country designations, and rules are subject to change.

-

The Differences Between 3PL and 4PL

It can be difficult to understand the intricacies between 3PL and 4PL. Don’t worry, we’re here to help.

-

What to Know About Incoterms® 2020

Incoterms rules guide international business leaders and clarify each party’s responsibilities during a supply chain transaction.